India classifies textile fabrics under three main chapters of the Customs Tariff Act: woven cotton fabric under Chapter 52, knitted fabric under Chapter 60, and silk and man-made filament fabrics under Chapters 50 and 54 respectively. GST on all textile fabric is 5%. Basic Customs Duty on fabric imports is 20% with Social Welfare Surcharge at 10% of BCD.

The first decision in any fabric classification is construction method: woven, knitted, or filament. Get that wrong and the chapter will be wrong.

What are the HSN codes for textile fabrics in India?

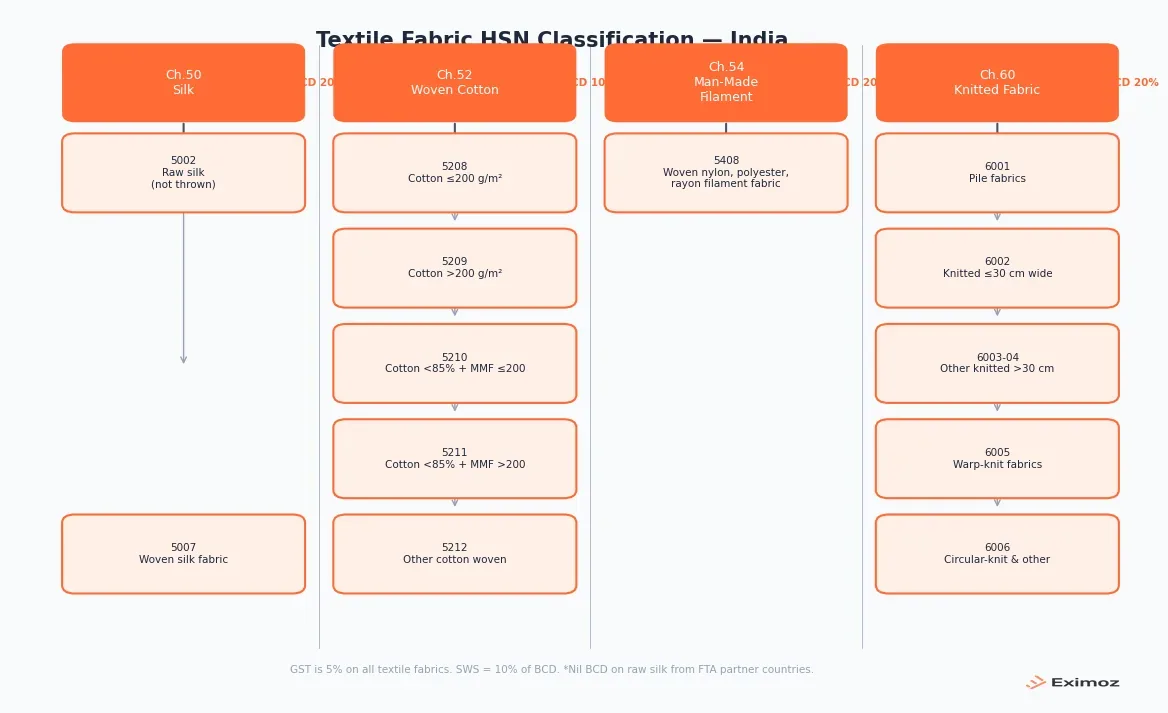

The HSN codes for textile fabrics in India fall across four chapters of the Customs Tariff Act: Chapter 52 for woven cotton, Chapter 60 for knitted fabric, Chapter 50 for natural silk, and Chapter 54 for man-made filament fabrics.

Chapter 52 covers woven cotton fabric. Sub-headings 5208 through 5212 cover different weight ranges and processing stages (unbleached, bleached, dyed, printed).

Chapter 60 covers knitted fabric. This includes warp-knit, circular-knit, and pile fabrics under headings 6001 through 6007.

Chapter 50 covers natural silk fabric including woven silk fabric under 5007.

Chapter 54 covers man-made filament fabric, primarily woven nylon, polyester, and rayon fabrics under heading 5408.

Woven fabric goes to Chapter 52 or 54. Knitted fabric goes to Chapter 60. Natural silk fabric goes to Chapter 50. Misclassifying knitted as woven is one of the most common errors in fabric customs clearance.

What is the HSN code for woven cotton fabric?

Woven cotton fabric falls under Chapter 52, headings 5208 through 5212. The sub-classification depends on two factors: the weight of the fabric per square metre and the processing stage.

Weight per square metre is the first split. Fabrics weighing 200 g/m² or less fall under heading 5208. Fabrics weighing more than 200 g/m² fall under heading 5209.

Processing stage further divides each heading. Within 5208, unbleached fabric is 5208.11, bleached is 5208.21, dyed is 5208.31, and printed is 5208.41. The same fourth-digit pattern applies to 5209 and the other headings.

Cotton fabrics mixed with man-made fibres (where cotton is below 85%) fall under heading 5210 (for fabrics 200 g/m² or less) or 5211 (for fabrics over 200 g/m²). Heading 5212 catches any other cotton woven fabrics, including quilted products.

| Fabric Type | Chapter | HSN Headings | GST | BCD (Imports) | SWS | Notes |

|---|---|---|---|---|---|---|

| Woven cotton fabric (≤200 g/m²) | 52 | 5208.xx.xx | 5% | 10% | 10% of BCD | Sub-divided by unbleached/bleached/dyed/printed |

| Woven cotton fabric (>200 g/m²) | 52 | 5209.xx.xx | 5% | 10% | 10% of BCD | Same sub-divisions |

| Cotton mixed with MMF (≤200 g/m²) | 52 | 5210.xx.xx | 5% | 10% | 10% of BCD | <85% cotton with man-made fibres |

| Other cotton fabrics | 52 | 5211.xx.xx, 5212.xx.xx | 5% | 10% | 10% of BCD | <85% cotton with MMF (>200 g/m²); includes quilted fabrics |

| Knitted cotton fabric | 60 | 6001-6007 | 5% | 20% | 10% of BCD | Warp-knit, circular-knit, pile |

| Man-made filament fabric | 54 | 5408.xx.xx | 5% | 20% | 10% of BCD | Nylon, polyester, rayon woven |

| Silk woven fabric | 50 | 5007.xx.xx | 5% | 20% | 10% of BCD | Nil BCD for raw silk under some FTAs |

For customs clearance, the commercial invoice must carry the 8-digit HSN code. It should also specify the weight per square metre and the processing condition. Check the supplier's tech pack or fabric spec sheet for these details, they don't always appear on the commercial invoice.

What HSN code applies to knitted fabric?

Knitted fabric falls under Chapter 60, headings 6001 through 6007. The classification splits are based on width, pile type, and construction.

Heading 6001 covers pile fabrics, including long pile and looped pile fabrics. Heading 6002 covers knitted or crocheted fabrics of width 30 cm or less, typically elastic or narrow knitted fabrics. Headings 6003 and 6004 cover other knitted fabrics of width greater than 30 cm. Heading 6005 covers warp-knit fabrics and 6006 covers other circular-knit fabrics.

Warp-knit and circular-knit fabrics are often confused with each other. Warp-knit fabrics are produced using parallel yarns looped vertically. They include fabrics like lingerie Tricot and are typically in tube form or open-width. Circular-knit fabrics are produced from a continuous tube, common in fleece and sportswear. Getting the construction type wrong is a documentation error customs officers can flag.

Another common error: knitted fabric gets misclassified as woven fabric under Chapter 52. The two look similar in finished form, but the construction method is fundamentally different. If the fabric spec does not state "knitted" or "circular knit" or "warp knit," check the fabric construction directly.

How are silk and man-made filament fabrics classified?

Natural silk fabric falls under Chapter 50. Raw silk (not thrown) is classified under heading 5002. Woven silk fabric is under heading 5007, sub-divided by processing: unbleached at 5007.10, bleached at 5007.20, dyed at 5007.30, printed at 5007.40.

Man-made filament fabrics (nylon, polyester, rayon) are classified under Chapter 54, heading 5408. These are woven fabrics made from continuous filament yarns. The distinction from spun yarn fabrics (which fall under Chapter 55) is that filament fabrics use long continuous strands while spun yarn fabrics use short staple fibres spun into yarn.

BCD on silk fabric imports is 20%, though raw silk (heading 5002) attracts nil BCD under some of India's FTA schedules including from ASEAN member states. Verify the FTA schedule for the specific country of origin before calculating landed cost.

Man-made filament fabric under 5408 attracts 20% BCD and 5% GST. Standard FTA schedules do not provide concessional rates for these items.

What are the GST and customs duty rates on fabric imports?

The duty structure on fabric imports has three components.

Basic Customs Duty (BCD): 20% on CIF value for most woven and knitted fabric imports.

Social Welfare Surcharge (SWS): 10% of the BCD, effectively 2% of CIF.

IGST: 5% on the assessable value (CIF + BCD + SWS).

GST on all textile fabrics under the CGST Rate Schedule is 5%, regardless of whether the fabric is woven cotton, knitted cotton, silk, or man-made filament.

The total landed cost formula for most fabric imports:

Total Duty = BCD (20%) + SWS (2%) + IGST (5% on assessable value)

There is a structural GST inversion in the textile value chain worth knowing about. Yarn attracts 12% GST while fabric attracts 5%. A garment manufacturer buying fabric at 5% and selling garments at 12% has a positive GST credit position. For fabric importers, the 5% rate on fabric is an input advantage that does not always flow through cleanly; it depends on the garment price point.

For fabric exports, RoDTEP (Remission of Duties and Taxes on Exported Products) may apply, refunding certain embedded taxes. Check DGFT notifications for the specific fabric heading before filing.

What mistakes happen in fabric HSN classification?

Confusing knitted fabric (Chapter 60) with woven fabric (Chapter 52). Knitted and woven fabrics look similar in finished form. The classification must come from the construction method in the fabric spec, not the visual appearance.

Wrong weight band selection. The 200 g/m² threshold between 5208/5210 and 5209/5211 is a hard boundary. A fabric at 201 g/m² belongs in 5209, not 5208.

Blend ratio errors in mixed fibre fabrics. Cotton mixed with man-made fibres where cotton is below 85% falls under 5210 or 5211. If the actual cotton content is higher than declared, the customs officer may reclassify and demand additional duty.

Confusing man-made filament (Chapter 54) with spun yarn fabrics (Chapter 55). Chapter 54 is for continuous filament yarns woven into fabric. Chapter 55 is for spun staple fibre fabrics. Polyester filament fabric (Chapter 54) is different from polyester spun fabric (Chapter 55). The yarn type determines the chapter.

Silk waste falls under Chapter 50. Cotton waste falls under Chapter 52. Both are waste or by-product classifications but in different chapters. A consignment with both silk waste and cotton fibre waste needs separate line items with the correct chapter for each.

Frequently Asked Questions

What are the HSN codes for woven cotton fabric in India?

Woven cotton fabric HSN codes fall under Chapter 52, headings 5208 through 5212. Heading 5208 covers plain weave fabrics of cotton 85% or more with weight 200 g/m² or less, sub-divided by processing: unbleached at 5208.11, bleached at 5208.21, dyed at 5208.31, printed at 5208.41. Heading 5209 covers pure cotton fabrics above 200 g/m². Heading 5210 covers cotton fabrics below 85% mixed with man-made fibres at weight 200 g/m² or less. Heading 5211 covers cotton fabrics below 85% mixed with man-made fibres above 200 g/m². (Pure cotton fabrics over 200 g/m² go under 5209.) Heading 5212 covers other cotton fabrics including quilted products. GST on woven cotton fabric is 5% and BCD is 10%.

What is the HSN code for knitted fabric in India?

Knitted fabric falls under Chapter 60, headings 6001 through 6007. Heading 6001 covers pile fabrics including long pile and looped pile. Heading 6002 covers knitted/crocheted fabrics of width 30 cm or less, typically elastic narrow fabrics. Headings 6003 through 6006 cover other knitted fabrics of width above 30 cm, with 6005 covering warp-knit fabrics and 6006 covering circular-knit and other knitted fabrics. GST on knitted fabric is 5% and BCD is 20%.

How is silk fabric classified under HSN?

Natural silk fabric falls under Chapter 50. Raw silk (not thrown) is classified under heading 5002. Woven silk fabric is under heading 5007, sub-divided by processing: unbleached at 5007.10, bleached at 5007.20, dyed at 5007.30, printed at 5007.40. Man-made filament fabrics (nylon, polyester, rayon woven) fall under Chapter 54 heading 5408. GST on silk fabric is 5% and BCD on silk fabric imports is 20%, though nil BCD applies to raw silk from countries covered by India's FTA schedules.

What is the customs duty on fabric imports to India?

BCD on most fabric imports (woven or knitted) is 20%. India's Free Trade Agreements with ASEAN, Japan, Korea, and other partner countries provide nil or concessional BCD on certain fabric imports from those countries. Social Welfare Surcharge is 10% of BCD. IGST is 5% on the assessable value which includes CIF, BCD, and SWS. Anti-dumping duty may apply to certain fabrics from specific countries; check DGTR for current investigations.

What is the GST rate on fabric in India?

GST on all textile fabrics, whether woven cotton, knitted cotton, silk, or man-made filament, is 5% under the CGST Rate Schedule. However, if the fabric is manufactured into garments, the GST changes to 12% for garments priced above Rs 1,000 per piece and 5% for garments priced at or below Rs 1,000 per piece. The GST inversion between fabric (5%) and garments (12% above Rs 1,000) creates a positive input tax credit position for most garment manufacturers.

India's textile sector is the world's second-largest by volume. If you import or trade fabric, correct HSN classification saves duty and avoids customs disputes that can hold up shipments at the port. Eximoz auto-classifies all fabric types and calculates the complete landed cost including BCD, SWS, and IGST before you place a purchase order. Find out more at eximoz.com.

FAQ Schema (JSON-LD)

{

"@context": "https://schema.org",

"@type": "FAQPage",

"mainEntity": [

{

"@type": "Question",

"name": "What are the HSN codes for woven cotton fabric in India?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Woven cotton fabric HSN codes fall under Chapter 52, headings 5208 through 5212. Heading 5208 covers cotton fabrics 85%+ with weight ≤200 g/m² (unbleached 5208.11, bleached 5208.21, dyed 5208.31, printed 5208.41). Heading 5209 covers pure cotton fabrics >200 g/m². Heading 5210 covers cotton <85% mixed with MMF at ≤200 g/m². Heading 5211 covers cotton <85% mixed with MMF at >200 g/m². Heading 5212 covers other cotton fabrics including quilted. GST is 5% and BCD is 10% for Chapter 52 woven cotton fabrics."

}

},

{

"@type": "Question",

"name": "What is the HSN code for knitted fabric in India?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Knitted fabric falls under Chapter 60, headings 6001 through 6007. Heading 6001 covers pile fabrics. 6002 covers narrow knitted fabrics ≤30cm wide. 6003-6006 cover other knitted fabrics >30cm wide, with 6005 for warp-knit and 6006 for circular-knit and other knitted fabrics. GST is 5% and BCD is 20%."

}

},

{

"@type": "Question",

"name": "How is silk fabric classified under HSN?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Natural silk fabric falls under Chapter 50. Raw silk is 5002. Woven silk fabric is 5007 (unbleached 5007.10, bleached 5007.20, dyed 5007.30, printed 5007.40). Man-made filament fabrics (nylon, polyester, rayon woven) fall under Chapter 54 heading 5408. GST is 5% on silk. BCD is 20%, with nil BCD on raw silk under some FTA schedules."

}

},

{

"@type": "Question",

"name": "What is the customs duty on fabric imports to India?",

"acceptedAnswer": {

"@type": "Answer",

"text": "BCD on most fabric imports is 20%. FTA partner countries (ASEAN, Japan, Korea and others) may get nil or concessional BCD. SWS is 10% of BCD. IGST is 5% on assessable value (CIF + BCD + SWS). Anti-dumping duty may apply to certain fabrics from specific countries."

}

},

{

"@type": "Question",

"name": "What is the GST rate on fabric in India?",

"acceptedAnswer": {

"@type": "Answer",

"text": "GST on all textile fabrics is 5% under CGST Rate Schedule, whether woven cotton, knitted, silk, or man-made filament. For garments made from those fabrics, GST is 12% if priced above Rs 1,000 per piece and 5% if at or below Rs 1,000 per piece. The 5% fabric / 12% garment structure creates a positive input tax credit for garment manufacturers."

}

}

]

}

Sources:

- CBIC Customs Tariff, Chapter 52 (Cotton fabrics): https://www.cbic.gov.in/htdocs-cbec/customs/cs-act/formatted-htmls/cs-tariff2025-26/chap-52.pdf

- CBIC Customs Tariff, Chapter 60 (Knitted fabrics): https://www.cbic.gov.in/htdocs-cbec/customs/cs-act/formatted-htmls/cs-tariff2025-26/chap-60.pdf

- CBIC Customs Tariff, Chapter 54 (Man-made filament): https://www.cbic.gov.in/htdocs-cbec/customs/cs-act/formatted-htmls/cs-tariff2025-26/chap-54.pdf

- CBIC GST Rate Schedule: https://cbic-gst.gov.in/gst-goods-services-rates.html

- DGFT Trade Notices: https://www.dgft.gov.in/CP/?opt=tradnotice