The HSNS (Health Security se National Security) Cess is a capacity-based levy effective February 1, 2026, applicable exclusively to manufacturers and importers of Pan Masala (CTH 2106 90 20). It replaces the GST Compensation Cess, charges cess based on installed machine capacity — not actual sales — and requires mandatory monthly advance payment by the 7th of each month via the CBIC Taxpayer Portal.

What Is HSNS Cess and Why Was It Introduced?

The GST Compensation Cess was a temporary levy designed to compensate Indian states for revenue shortfall during the GST transition period. When that compensation period ended, the Centre needed a new revenue mechanism. The HSNS Cess fills that gap — and unlike its predecessor, it is explicitly directed toward two spending categories: national security and public health.

The cess is independent of GST. Paying your GST does not reduce or substitute your HSNS Cess liability. Both levies apply simultaneously. The HSNS Act, 2025 also gives the Centre the power to notify additional goods — but as of now, only Pan Masala attracts HSNS Cess.

"A dedicated, reliable revenue stream to support expenditure on National Security and Public Health." — PIB Press Release

Who Is Liable to Pay HSNS Cess — Manufacturers, Importers, or Both?

Both manufacturers and importers are liable.

Every person manufacturing or producing Pan Masala in India must register and pay. Importers of Pan Masala into India are equally subject to the cess — it applies at the customs barrier, making it a cost layer in your landed cost calculation.

Crucially: GST registration does NOT cover HSNS Cess. A separate registration on the CBIC Taxpayer Portal is mandatory. Non-registration is a prosecutable offence.

| Parameter | Detail |

|---|---|

| Effective Date | February 1, 2026 |

| Governing Legislation | HSNS Cess Act, 2025 |

| Currently Applicable Goods | Pan Masala only (CTH 2106 90 20) |

| Tax Rate | Capacity-based (Schedule II — varies by machine type and capacity) |

| GST on Pan Masala | 40% (in addition to HSNS Cess) |

| Registration | Mandatory on CBIC Taxpayer Portal (separate from GST registration) |

| Payment Due Date | 7th of every month (advance payment) |

| First Amendment Rules | Effective February 1, 2026 — clarified RPM and gear ratio calculations |

| Latest Advisory | Advisory No. 07/2026 (April 17, 2026) — Amendment Declaration filing |

| Compounding | 50–150% of cess for minor offences; not for repeat offenders |

| Recovery Timeline | 24 months from return filing date |

| Adjudication Timeline | 1 year (extendable by 6 months) |

| Appellate Authority | CESTAT |

How Is HSNS Cess Calculated — Capacity vs. Sales-Based?

HSNS Cess is a capacity-based levy — not a sales-or-production-based one. Under Schedule II of the HSNS Cess Act, 2025, the cess is determined by the number, type, and capacity of your packing machines installed. Specifically: the RPM and gear ratios of each machine.

The actual quantity you manufacture is irrelevant. Cess liability is triggered as soon as your machine capacity falls within Schedule II thresholds — even for minimal or manual production runs.

The First Amendment Rules (effective February 1, 2026) clarified how RPM and gear ratios are used to calculate installed capacity. If any of your machines have been completely non-operational for 15 or more consecutive days, you may claim abatement — but this requires verification by the proper officer.

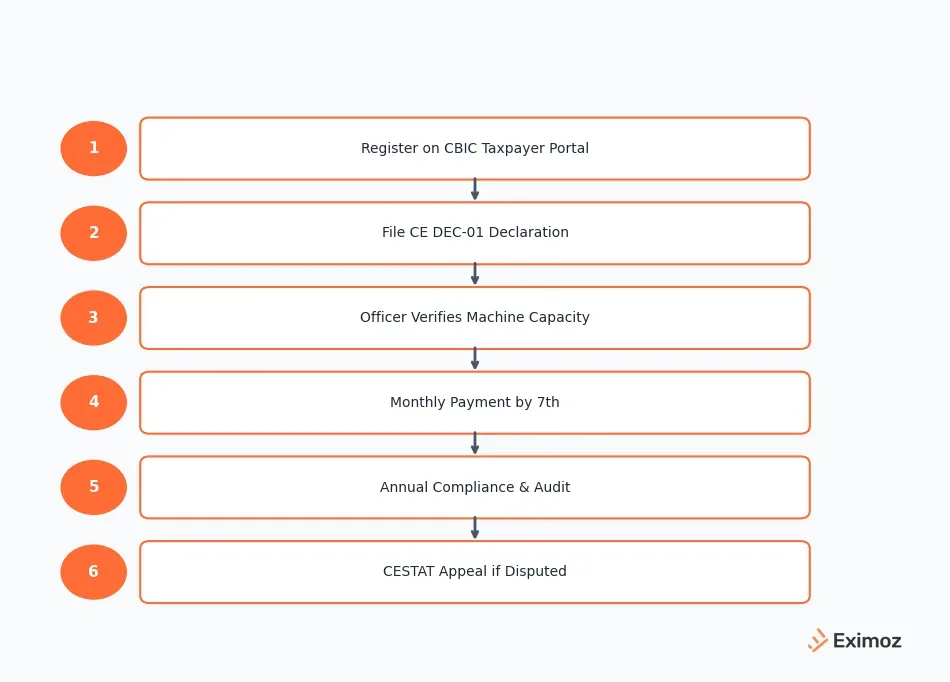

HSNS Cess Registration and Payment: Step-by-Step

- Log in to the CBIC Taxpayer Portal at cbic-gst.gov.in. If you do not already have an account, create one separately — your GST credentials do not auto-grant access here.

- Navigate to Registration → File Declaration (CE DEC-01 Form).

- Declare your installed machine capacity — number of machines, type, RPM, and gear ratios.

- Proper officer verifies your declaration. The officer is separately notified by the government.

- Pay the cess in advance every month by the 7th. For example: February 2026 cess was due by February 7, 2026.

Figure 1: HSNS Cess compliance process — from CBIC registration to CESTAT appeal

Compliance Risks, Penalties, and Recent Updates

- Non-registration: prosecutable offence with penalties under the HSNS Cess Act

- Compounding: 50–150% of cess for minor first offences — but NOT available for repeat offenders

- Recovery of unpaid cess: initiated within 24 months from the date of filing the return

- Adjudication: must be completed within one year, extendable by six months

- Appellate route: designated Appellate Authority → CESTAT → High Court → Supreme Court

Latest update: Advisory No. 07/2026 (April 17, 2026) covers the Amendment Declaration filing procedure — importers and manufacturers should review this alongside the original advisories.

Frequently Asked Questions

What is HSNS Cess in India and which goods does it apply to?

The Health Security se National Security (HSNS) Cess is a standalone statutory levy under the HSNS Cess Act, 2025, effective February 1, 2026. It currently applies only to Pan Masala (CTH 2106 90 20). The government may notify additional goods in the future, but no cess applies to any product without explicit notification. The cess is charged in addition to the 40% GST on Pan Masala and all other applicable taxes.

Is HSNS Cess applicable to importers of Pan Masala, or only to domestic manufacturers?

HSNS Cess applies to every person who manufactures or produces Pan Masala in India and is liable to pay the cess. Importers of Pan Masala into India are also subject to the cess on the customs side, and both manufacturers and importers must register on the CBIC Taxpayer Portal and make advance monthly payments by the 7th of each month.

How is HSNS Cess calculated — is it based on actual production or capacity?

HSNS Cess is a capacity-based levy, not a sales-or-production-based levy. Under Schedule II of the HSNS Cess Act, 2025, the cess is determined by the number, type, and capacity of packing machines installed. The actual quantity manufactured is irrelevant — cess liability is triggered as soon as machine capacity falls under Schedule II thresholds, even for manual production. The First Amendment Rules (effective February 1, 2026) clarified machine capacity calculation using RPM and gear ratios.

What is the HSNS Cess registration and payment process on the CBIC portal?

Step 1: Register on the CBIC Taxpayer Portal at cbic-gst.gov.in (separate from GST registration). Step 2: File a declaration of installed machine capacity using CE DEC-01 Form under the Registration menu. Step 3: The proper officer verifies your machine declaration. Step 4: Pay the cess amount in advance every month by the 7th of the following month. For example, HSNS Cess for February 2026 was due by February 7, 2026.

What are the penalties for non-registration or non-payment of HSNS Cess?

Non-registration under the HSNS Cess Act is an offence attracting prosecution and penalties. Compounding of minor offences is available at 50–150% of the cess involved, but this is not available for repeat offenders. Recovery of unpaid cess can be initiated within 24 months from the date of filing the return. Adjudication must be completed within one year, extendable by six months.

HSNS Cess represents a fundamental shift from sales-based to capacity-based taxation for Pan Masala manufacturers and importers. The live regulatory updates — most recently Advisory 07/2026 in April — mean compliance teams must actively track CBIC advisories. For automated tracking of regulatory deadlines and multi-cess visibility, Eximoz helps trade compliance teams stay ahead — eximoz.com