The HSN code for paint in India falls under Chapter 32 of the Customs Tariff Act, 1975. Solvent-based paints (oil-based, alkyd, polyurethane) are classified under heading 3208. Water-based paints (emulsion, latex, acrylic) go under heading 3209. GST on all paints is 18%, and Basic Customs Duty on imported paints is 10%.

What is the HSN code for paint in India?

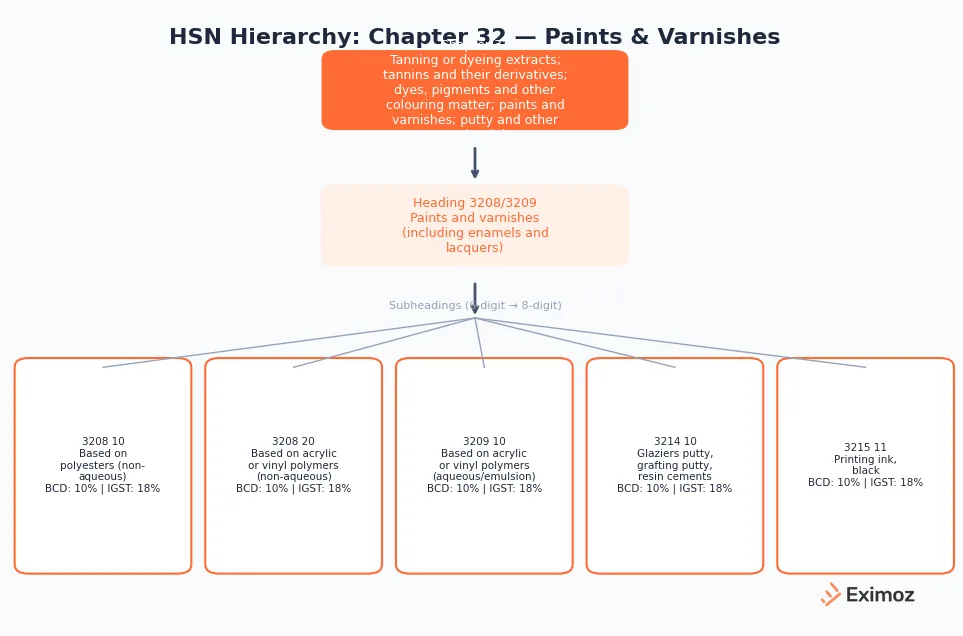

All paints, varnishes, enamels, and lacquers are classified under Chapter 32 of the Customs Tariff:

- 3208: Non-aqueous (solvent-based) paints: oil-based, alkyd, polyurethane, and epoxy.

- 3209: Aqueous (water-based) paints: emulsion, latex, and acrylic coatings.

- 3210: Other paints and varnishes, including distemper.

- 3213: Artists' colours in sets, tubes, pans, or bottles.

- 3214: Putty, resin cements, caulking compounds, and painters' fillers.

- 3215: Printing ink, writing ink, and other inks.

The 4-digit heading depends on whether the paint uses water or organic solvent as its dispersion medium. The 8-digit code narrows further by polymer type.

How are emulsion and oil-based paints classified differently?

Water-based (HSN 3209): Emulsion, latex, and acrylic coatings. If water is the primary medium, the product goes under 3209 regardless of polymer. Acrylic and vinyl emulsions both fall under 3209 10.

Solvent-based (HSN 3208): Oil-based, alkyd, polyurethane, and epoxy paints. If the medium is an organic solvent (turpentine, mineral spirits, xylene), it falls under 3208. Automotive and industrial primers classify under 3208 20.

Misclassifying between these headings triggers a different tariff line. The GST rate is 18% for both, but the 8-digit codes affect ITC matching and export documentation.

| Paint Type | HSN Code | BCD Rate | IGST Rate | GST Rate |

|---|---|---|---|---|

| Emulsion paint | 3209 10 | 10% | 18% | 18% |

| Oil-based paint | 3208 10 | 10% | 18% | 18% |

| Primers | 3208 20 | 10% | 18% | 18% |

| Varnishes | 3208 90 | 10% | 18% | 18% |

| Lacquers | 3208 90 | 10% | 18% | 18% |

| Putty/fillers | 3214 10 | 10% | 18% | 18% |

| Distemper | 3210 00 | 10% | 18% | 18% |

| Artists' paints | 3213 | 10% | 18% | 18% |

| Printing ink | 3215 | 10% | 18% | 18% |

| Automotive paint | 3208 20 | 10% | 18% | 18% |

Source: CBIC Customs Tariff and GST Rate Schedule, FY 2025-26.

Figure 1: HSN code hierarchy for paints and varnishes under India's Customs Tariff — Chapter 32.

What GST and customs duty rates apply to paints?

GST on all paints under Chapter 32 is 18%, reduced from 28% effective July 27, 2018 (28th GST Council meeting). No compensation cess applies.

For imports, the duty structure is:

Basic Customs Duty (BCD): 10%

Social Welfare Surcharge (SWS): 10% of BCD (i.e., 1% of assessable value)

IGST: 18% on (assessable value + BCD + SWS)

Effective total import duty: ~31%

Verify rates for a specific shipment on the IceGate Customs Duty Calculator. Printing ink (HSN 3215) was raised from 12% to 18% GST in July 2022 via Notification No. 03/2022-Central Tax (Rate).

How are automotive and industrial coatings classified under HSN?

Classification is based on composition, not the surface being painted:

- Automotive OEM paints: Solvent-based, under 3208 20.

- Marine coatings: Anti-fouling and anti-corrosion, under 3208 90.

- Powder coatings: Under 3208 90 (film forms from non-aqueous polymer).

- Anti-corrosion primers: 3208 10 or 3208 20 depending on polymer base.

- Road-marking paints: Under 3210 00.

What are common classification mistakes for paint products?

- Emulsion vs distemper. Emulsion paint (3209) is polymer-based; distemper (3210) is chalk-based. Different headings.

- Artists' colours vs industrial paint. Artists' paints in tubes or sets fall under 3213, not 3208/3209.

- Printing ink vs paint. Printing ink (3215) and paint (3208/3209) are classified separately.

- Putty as paint. Putty and caulking compounds go under 3214, not paint headings.

- Spray paint by container. Aerosol paint is classified by contents, not the can. Spray enamel is still 3208.

Each error leads to BoE amendments, delayed clearance, and duty reassessment.

Frequently Asked Questions

What is the GST rate on paint in India?

All paints and varnishes attract 18% GST, including emulsion, oil-based, industrial, automotive, primers, putty, lacquers, and distemper under Chapter 32. Reduced from 28% to 18% on July 27, 2018. Printing ink (HSN 3215) was raised from 12% to 18% in July 2022. No compensation cess applies.

What is the HSN code for emulsion paint?

Water-based emulsion paints fall under HSN 3209. Acrylic and vinyl emulsions are classified under 3209 10. GST is 18%, BCD on imports is 10%. Distemper falls under a separate heading (3210), not 3209.

What is the difference between HSN 3208 and 3209?

HSN 3208 covers non-aqueous (solvent-based) paints; HSN 3209 covers aqueous (water-based) dispersions. The polymer type does not determine the heading; only the solvent does. Both carry 10% BCD and 18% GST, but the wrong code creates ITC mismatches and can trigger audit scrutiny.

What customs duty applies on importing paint into India?

Imported paints attract 10% BCD, 10% Social Welfare Surcharge on BCD, and 18% IGST on assessable value plus BCD plus surcharge. Effective total duty is approximately 31%. Anti-dumping duty may apply on specific raw materials (e.g., titanium dioxide from China). Verify rates on the IceGate Customs Duty Calculator.

How are paint raw materials like pigments and thinners classified?

Pigments fall under 3204 (synthetic organic colouring matter) or 3206 (including titanium dioxide). Thinners and solvents are under Chapter 29 or 3814 (composite solvents). Putty and fillers are under 3214. Each has its own GST rate, though many attract 18%.

Paint classification looks straightforward at the 4-digit level, but raw material inputs across Chapters 29, 32, and 38 each carry their own duty and GST treatment. Eximoz automates HSN classification for paint manufacturers and importers, mapping your complete input basket to the correct codes for accurate costing and ITC claims. Worth checking if you handle high volumes: eximoz.com