The Duty Drawback Scheme under Sections 74 and 75 of the Customs Act, 1962 allows Indian exporters to claim a refund of customs duties paid on imported materials used in manufacturing exported goods. Section 74 covers re-export of imported goods (up to 98% refund within 2 years), while Section 75 covers drawback on materials used in manufacturing export products, either through All Industry Rates (AIR) or Brand Rates published by CBIC.

What is duty drawback and how does it work?

Duty drawback lets Indian exporters recover customs duties paid on imported inputs that go into making exported products. Its legal basis is Sections 74 and 75 of the Customs Act, 1962.

The logic is simple: you import raw materials, pay customs duty, use those materials to manufacture goods for export, and the government refunds the duty. This removes the embedded duty cost from your export pricing.

It covers Basic Customs Duty (BCD), the customs component of IGST, and education cess. How you claim depends on whether you're re-exporting imported goods as-is (Section 74) or exporting manufactured products that used imported inputs (Section 75).

What is the difference between Section 74 and Section 75 drawback?

People mix these up all the time.

Section 74 applies when you import goods and re-export them, either unused or with only minor use. If you import industrial equipment for a project, the project gets cancelled, and you ship the equipment back, you can claim up to 98% of the duty paid. You must re-export within 2 years of the original import date. The refund decreases based on usage, following a depreciation schedule published by CBIC.

Section 75 is what most exporters actually use. It applies when imported raw materials go into manufacturing a product that gets exported. If you import cotton yarn, manufacture garments, and export them, Section 75 is your route. The rates are either All Industry Rates (AIR), which are fixed percentages, or Brand Rates, calculated based on actual duty-paid inputs.

| Feature | Section 74 (Re-export) | Section 75 (Manufacturing) |

|---|---|---|

| Purpose | Refund on re-exported imported goods | Refund on inputs used in export manufacturing |

| Goods covered | Imported goods exported as-is | Raw materials/inputs used in manufactured exports |

| Refund percentage | Up to 98% of duty paid | As per AIR schedule or Brand Rate |

| Time limit | Re-export within 2 years | No time limit on manufacturing |

| Rate type | Depreciation-based schedule | All Industry Rate (AIR) or Brand Rate |

| Documents needed | Import BoE, Shipping Bill | Shipping Bill, import BoE, manufacturing records |

| Filing process | Claim at time of re-export | Declare on Shipping Bill, auto-credit after LEO |

Source: Sections 74 & 75, Customs Act, 1962 (CBIC Tax Information Portal)

What are the All Industry Drawback Rates for 2025-26?

CBIC publishes the All Industry Rates (AIR) every year. Each export tariff item has a fixed drawback rate, either a percentage of FOB value or a fixed amount per unit. The AIR schedule for 2025-26 covers thousands of categories.

AIR has two components: customs duty and central excise. Since GST, drawback covers only the customs duty portion for most products.

| Export Sector | Typical Drawback Rate (% of FOB) |

|---|---|

| Textiles (cotton garments) | 1.5% - 2.5% |

| Engineering goods (steel products) | 1.0% - 1.8% |

| Chemicals (organic) | 2.0% - 3.5% |

| Leather goods | 1.5% - 2.0% |

| Marine products | 1.5% - 2.5% |

There's a cap: if the drawback amount exceeds one-third of the market value of the exported goods, it gets limited to that one-third.

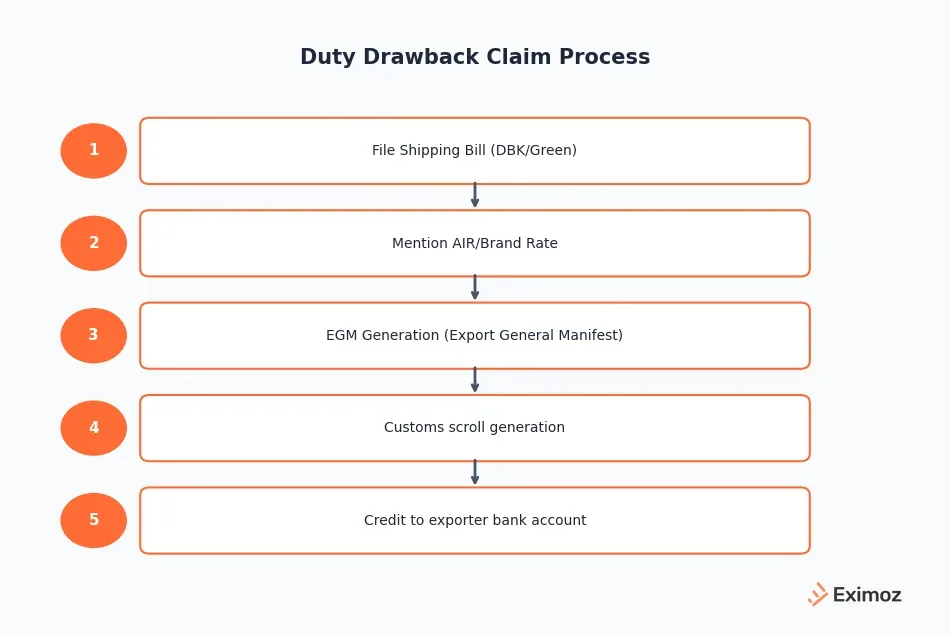

How to file a duty drawback claim step by step?

Filing happens through the EDI system at customs ports.

Step 1: Declare your drawback intent on the Shipping Bill. Select the drawback scheme on ICEGATE and enter the drawback serial number from the AIR schedule.

Step 2: Mention the correct drawback rate and tariff item number. If claiming Brand Rate, indicate that on the Shipping Bill.

Step 3: Get the Let Export Order (LEO) from the customs officer after examination.

Step 4: Once the goods are exported, the drawback amount is auto-credited to the designated bank account. For clean AIR claims, this happens within 7-15 days of the LEO date.

Step 5: Submit the Bank Realisation Certificate (BRC) within 3 months of export. Failure to submit the BRC leads to recovery of the drawback amount.

You'll need the Shipping Bill, import Bill of Entry, commercial invoice, packing list, and BRC. As per the Drawback Rules, 2017, claims not settled within the prescribed period attract 6% interest.

What is brand rate drawback and when should you use it?

Use Brand Rate when the All Industry Rate doesn't match the actual customs duty you paid on imported inputs. This comes up when your inputs carry higher-than-average duty or when the AIR has been set conservatively.

To get a Brand Rate, apply to the Drawback Directorate under CBIC with documentation of your actual imports, duties paid, manufacturing process, and input-output ratios.

It works in two stages. You apply for a provisional Brand Rate to claim drawback while the final rate is determined. Once verified, they fix a final Brand Rate and adjust any difference.

If your actual duty incidence is higher than what AIR gives you, Brand Rate is worth the extra paperwork. Chemicals and engineering exporters often find Brand Rate pays more than double what AIR would. The catch: Brand Rate claims need detailed manufacturing records and take 30-60 days to process, versus 7-15 days for AIR.

Frequently Asked Questions

What is the difference between duty drawback and RoDTEP?

Duty drawback refunds customs duties (BCD, IGST, excise on fuel) on imported inputs used in export manufacturing. RoDTEP reimburses embedded central, state, and local taxes that aren't otherwise refundable: electricity duty, mandi tax, stamp duty. You can claim both since they cover different cost layers.

How is duty drawback calculated?

Under All Industry Rates (AIR), the government publishes fixed drawback rates for each export product tariff item, expressed as a percentage of FOB value or a fixed amount per unit. Under Brand Rate, the calculation is based on actual import duties paid on inputs consumed in manufacturing the export product. Brand Rates are typically higher but require detailed documentation of your manufacturing process and input-output ratios.

How long does it take to receive a drawback refund?

AIR-based claims clear within 7-15 days of the LEO date if your documents are in order. Brand Rate claims take 30-60 days. Supplementary claims or anything requiring manual verification can stretch to 3-6 months.

Can a merchant exporter claim duty drawback?

Merchant exporters who buy from manufacturers and export can claim duty drawback, provided the Shipping Bill mentions the drawback claim and the supporting manufacturer's invoice shows the duty element. However, the drawback rate for merchant exporters may be lower if the manufacturer has already taken GST input tax credit on the imported inputs.

What happens if drawback goods are returned or rejected?

If exported goods covered by a drawback claim are returned to India, the exporter must repay the drawback amount within 30 days of re-import. The re-imported goods can be cleared by paying applicable customs duty. If the goods are repaired or reconditioned and re-exported, a fresh drawback claim can be made on the subsequent export.

Working out whether AIR or Brand Rate gives you better drawback on each shipment gets complicated, especially when input costs and duty rates shift. Eximoz runs both calculations based on your actual duty-paid inputs and recommends the best claim path for each export shipment. If your team handles high volumes and wants to stop leaving drawback money on the table, take a look at eximoz.com.