CBIC publishes a customs exchange rate every fortnight. This rate determines the rupee value used to calculate import duty on every Bill of Entry filed in India. If you're clearing goods through Indian customs, this rate is not optional — it is what your entire duty calculation runs on.

What Is a Customs Exchange Rate and Why Does CBIC Set It?

When you import goods, your commercial invoice is in a foreign currency. Indian customs needs that figure in rupees to calculate your duties. CBIC bridges this gap by issuing a standardised exchange rate every fortnight, sourced from the RBI Reference Rate published by the Financial Benchmarks India Private Limited (FBIL).

The legal basis is Section 14 of the Customs Act, 1962, which requires that the value of imported goods be expressed in Indian currency. CBIC does this through Customs (N.T.) notifications — one for each fortnight — published on the Press Information Bureau (PIB) and on CBIC's own website.

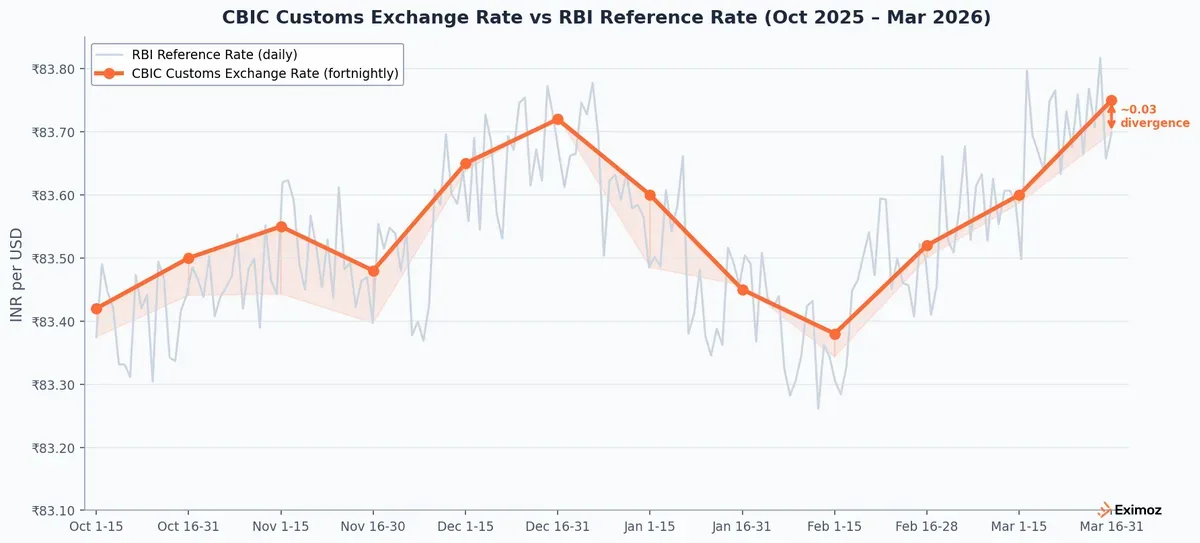

One thing that trips people up: the CBIC customs rate is not the same as the RBI Reference Rate you see in financial news. The RBI rate reflects interbank forex market conditions and is what banks use for their own transactions. CBIC derives its rate from the RBI figure but sets it aside specifically for customs duty computation. The two can and do differ on any given day, and that difference directly affects what you pay in duties.

How CBIC Determines the Customs Exchange Rate

CBIC runs a structured, time-bound cycle.

The source is the RBI Reference Rate published daily by FBIL on the RBI website. CBIC takes the RBI Reference Rate for the last working day of the preceding fortnight as the basis for its customs rate notification.

The fortnightly cycle works like this: CBIC issues a notification covering the 1st to the 15th of each month, typically by the 15th of the month before. A second notification covers the 16th through end of month, issued by the last working day of the first fortnight. This gives importers advance notice of which rate will apply during the upcoming period.

You can find the notification through several channels. The CBIC entities page at https://www.cbic.gov.in/Exchange-Rate-Notifications is the primary source. IceGate has an Exchange Rate Automation Module where the applicable fortnight rate is pre-populated at the time of filing. DGFT circulars and PIB press releases carry the same details.

The rate covers major trading currencies — USD, EUR, GBP, JPY, CNY, and others. The rate that applies to your Bill of Entry is the one in force on the date you file the BoE at the customs station, not the date your goods shipped or the date they arrived at the port.

How the Customs Exchange Rate Affects Your Import Duty Calculation

The customs exchange rate applies to the assessable value of your goods as declared on the Bill of Entry. Every component of your duty calculation — BCD, SWS, IGST — runs off the rupee figure produced by converting your invoice value at the CBIC rate.

Here is a worked example.

Assume a consignment of industrial machinery under Chapter 84 with a CIP value of USD 10,000. The CBIC customs rate for the applicable fortnight is INR 83.50 per USD. The RBI Reference Rate on the same day is INR 83.45 per USD.

Step 1: Convert invoice value to INR using the CBIC customs rate. USD 10,000 × INR 83.50 = INR 8,35,000

Step 2: Calculate Basic Customs Duty (BCD). For this machinery category, the applicable BCD rate is 7.5%. BCD = INR 8,35,000 × 7.5% = INR 62,625

Step 3: Calculate Social Welfare Surcharge (SWS). SWS = INR 62,625 × 10% = INR 6,262.50

Step 4: Calculate IGST on the cumulative value (CIF + BCD + SWS). Assessable value = INR 8,35,000 + INR 62,625 + INR 6,262.50 = INR 9,03,887.50 IGST at 18% = INR 9,03,887.50 × 18% = INR 1,62,699.75

Total customs duty = BCD + SWS + IGST = INR 62,625 + INR 6,262.50 + INR 1,62,699.75 = INR 2,31,587.25

If the importer had used the RBI trading rate of INR 83.45 instead, the assessable value would have been INR 8,34,500 — and the duty figure would be marginally different. Across hundreds of consignments, that gap compounds.

The rate that always applies is the CBIC customs rate in force on the BoE filing date. If goods arrive mid-fortnight and the BoE is filed within the same fortnight, the rate from that fortnight applies — even if the shipment left in the previous fortnight.

CBIC publishes a fortnightly customs exchange rate; RBI publishes a daily reference rate. The two diverge slightly throughout the period, affecting import duty calculations.

CBIC vs. RBI Exchange Rate: What Is the Difference?

| CBIC Customs Exchange Rate | RBI Reference Rate | |

|---|---|---|

| Source | Derived from FBIL/RBI rate | Published by RBI via FBIL |

| Purpose | Customs duty calculation | Forex market transactions |

| Frequency | Fortnightly notification | Daily publication |

| Used by | Customs authorities at BoE filing | Banks, financial institutions |

| Legally required for | Duty calculation | Not applicable for customs |

The two rates serve different purposes. The RBI rate is what banks use for forex dealings and currency conversion for trade settlements. The CBIC rate is an administrative rate derived from it and used only for customs duty computation.

How to Check and Download the Current CBIC Customs Exchange Rate

CBIC makes the rate available through four official channels.

The CBIC entities page at https://www.cbic.gov.in/Exchange-Rate-Notifications carries the current and historical rate notifications in a tabular format, updated with every fortnightly notification.

The IceGate portal at https://www.icegate.gov.in has an Exchange Rate Automation Module. When you file a Bill of Entry through IceGate, the system automatically fetches and displays the applicable CBIC customs rate for your filing date — no manual lookup required for routine clearances.

DGFT circulars and trade notices at https://www.dgft.gov.in often carry the CBIC notification details alongside policy updates that affect duty calculations.

PIB press releases at https://www.pib.gov.in publish the full text of each CBIC customs (N.T.) notification as it is issued — an official record with the exact rate and effective period.

For importers handling large volumes of SKUs, subscribing to CBIC and IceGate notification alerts is worth the setup. A rate shift in a fortnight can materially change duty projections for upcoming clearances. Knowing the rate before you file — not after — keeps your cost estimates honest.

Common Mistakes Importers Make with Customs Exchange Rates

Using the shipment date rate instead of the BoE filing date rate. The shipment date, arrival date, and invoice date are all irrelevant for customs exchange rate purposes. Only the BoE filing date determines which fortnightly rate applies. Importers who track shipments by departure dates routinely prepare wrong duty estimates.

Filing BoE after the allowed window. Section 46 of the Customs Act (as amended by the Finance Act, 2021) requires importers to file the Bill of Entry before the end of the day preceding the day of arrival of goods at the customs station. This is the advance filing mandate — BoE must be filed before goods arrive. Exception: for short-haul shipments arriving from neighbouring countries, BoE may be filed by end of the day of arrival. Under the old rule (before the 2021 amendment), BoE could be filed by the end of the next day after arrival, with a penalty of Rs. 5,000 per day for the first three days of default. Under the current advance filing rule, any BoE filed on or after the day of arrival — without a valid neighbouring-country exception — is treated as late and attracts penalty proceedings. Always plan for advance filing; there is no extended window.

Letting a new fortnight rate slip in mid-clearance. If your BoE filing gets delayed past the fortnight boundary, you must update the BoE to reflect the correct rate for the actual filing date. An BoE filed with a stale rate will get flagged at assessment.

Using the RBI trading rate instead of the CBIC customs rate. This is the most common error among importers who handle their own forex. The RBI rate on your bank statement or from a forex dealer is not the customs rate. Using it for duty calculation is wrong and will produce an incorrect liability figure.

Frequently Asked Questions

Who notifies the customs exchange rate in India?

CBIC notifies customs exchange rates fortnightly via Customs (N.T.) notifications, sourced from the RBI Reference Rate published by FBIL. Each notification covers one fortnight — either the 1st to the 15th or the 16th through end of month.

Is the CBIC customs exchange rate the same as the RBI reference rate?

No. The RBI Reference Rate is used by banks and financial institutions for forex market transactions. CBIC derives the customs rate from it but sets it aside exclusively for customs duty calculation, and the two rates may differ on any given day.

Which exchange rate applies for Bill of Entry filing — the shipment date or the arrival date?

Neither. The rate in force on the BoE filing date at the customs station is what applies. Shipment date and arrival date are not factors for customs exchange rate purposes.

Can importers use a rate lower than the CBIC customs rate?

No. Section 14 of the Customs Act, 1962 mandates that the CBIC notified exchange rate is the only valid rate for customs valuation purposes. There is no provision for importers to use a lower rate based on their actual bank transaction rate.

Where can I download the current CBIC customs exchange rate?

The official rate table is on CBIC's entities page at https://www.cbic.gov.in/Exchange-Rate-Notifications and in IceGate's Exchange Rate Automation Module at https://www.icegate.gov.in. DGFT circulars and PIB press releases also carry the notifications as they are issued.

Getting customs exchange rates right is one part of a broader compliance picture for importers handling high volumes. Every wrong rate assumption cascades into duty miscalculations that only surface at assessment or audit. Eximoz helps importers automate the customs compliance workflow — pre-filing checks on exchange rate applicability, BoE data validation, and duty calculation across multiple SKUs — before the consignment reaches the port.